Do you ever wonder why some industries advance quicker than others? Why it takes so long for innovations to reach the mainstream? And why don’t we have a time machine or flying cars yet? Well, let’s take a look.

To understand why we don’t have access to the best technology that exists, we must first understand how businesses work. Externally, a business’s purpose is to drive innovation and raise the standard of living by providing great products and services. However, internally, a business’s ultimate goal is to earn a profit. The Economist’s Financial Management defines a business as “a commercial operation that provides products or services with the aim of making a profit for the benefit of its owners… A profit is an essential element of running a successful business. It is a trading surplus whereby the revenues earned exceed the costs.”

The best classification of a successful business is one that creates a sustainable superior return on investment (ROI). In order for businesses to earn revenue, they must have a great product at a price that people are willing to pay. To turn revenue into a profit, the business must create their product while spending less than they sell it for, resulting in a net positive income.

To maintain a competitive moat, businesses continuously innovate their product making them better and better. If you look at the history of any industry, products have naturally gotten better over the years due to competitors threatening to take over their business with an even better product.

Cars started out slow and fragile. They used to only work on good roads, they were uncomfortable and had very few additional features. Today, cars can practically drive themself while we relax in an air-conditioned cabin while getting massaged on our dual-density foam seats. Phones started out bulky, unportable, unreliable, expensive, and unappealing. Now, not only can we video-chat with anyone around the world, but we can listen to any song, watch any movie, or access any information in just the palm of our hand.

Technological innovation is great for consumers. As technology advances, prices drop and products get better. One of the main reasons technology gets cheaper over time is from advancements in manufacturing. Companies find new materials to use, or they build robots and machines to help make things faster and cheaper. They find new ways to put together the product and send it out in a cheaper way through supply chain redesign.

Competition is one of the biggest drivers of innovation. It forces companies to find ways of standing out and making their business more efficient. Companies are always looking for new innovations to improve their competitive moat, but some are just too expensive to implement. Although it may greatly improve their final product, some innovations aren’t economically feasible.

New innovations usually increase the cost to make the product, and as manufacturing costs go up, companies are forced to increase the price of the final product to protect their profit margin. Depending on how valuable the innovation is to customers and how much the price increases, the innovation could destroy the demand for the product. Usually, with commodity products or necessity goods, customers aren’t willing to pay much more for innovation. The trade-off just isn’t worth it. This explains why most of us still use the same broomstick technology since the 1800s. This innovation enigma is the reason so many innovations are left unborn in so many industries.

A large industry that lacks consumer-oriented innovation is healthcare. In the United States, employers pay over 80% of our insurance, which then pays for our medical bills. If you go to a clinic and receive sub-par service, you often don’t have the power to change clinics because of insurance policy restrictions, or because there aren’t any other clinics nearby. Because we have limited options, healthcare providers aren’t pressured to innovate for the customer. Instead, they’re incentivized to please the ones who pay them—employers and the government.

Industries that are pressured by consumers benefit them a lot more. In ancient times, Blackberry phones were the hottest tech in the early 2000s, until Apple and Samsung released slimmer phones with touchscreen technology, HD cameras, and better features. From there, it became survival of the fittest. Whoever could provide the best product for the best value for the price, wins. And whoever fails to impress and satisfy, dies (RIP Nokia, Blackberry, Motorola).

There are many examples of cool technology that exist but are unaffordable to the average consumer or are sold as one-of-one products because of the manufacturing complexities. Carbon fiber is 5x stronger and twice as stiff as steel, extremely light, resistant to corrosion, and has tons of other benefits making it perfect for vehicles, sporting goods, aerospace, and many other things. However, the processing and manufacturing process is very difficult and thus costly. Because of this, carbon fiber is only seen on luxury and one-off products where producers can afford to raise the price without hurting demand.

One-off production naturally tends to be avoided as a business model due to the massive expenses and the unrepeatable nature of the product. Usually, to bring a new product to market, it needs to pass through a number of stages, each requiring significant capital and different experts. First, fundamental science is used to understand the underlying functionality of a tool. Then, engineers use the known science to hypothesize the bounds of the tools’ functionality. Engineers also create a means of production of such tools which also takes time and money to develop. If a customer hasn’t placed a downpayment on the product beforehand, then marketing is needed to convince a customer of the value of the innovation. When a product is one-off it requires all these extra costs for something that won’t be repeated. Unless it’s a strategic bespoke product then a business that only sells one-off products is either not very unique (like a type of art business) or isn’t scalable.

Another reason we may not have access to the best technology is that it’s protected as a competitive advantage. In the private sector, this happens through patents where a company reserves the exclusive right to produce a technology for a period of twenty years. In the public sector, governments seek to have the best military, security, communication, vehicles, and anything else that can help protect and serve their country. The US government, with trillions of dollars in annual spending power, is able to acquire bespoke products with the most efficient material and technology because they can afford to pay for the extra costs that come with it. The Lockheed SR-71 “Blackbird” is an incredible showcase of technology. It is a jet that can cruise near the edge of space and outfly a missile (even faster than a bullet, 2,193 mph). To this day, it holds the records for the fastest and highest-flying aircraft ever—and it was released in 1966 which is over half a century ago. Just think what technology the government has access to today in 2021…

For technology to advance and reduce cost, it needs two things. Firstly, a moonshot innovation needs foundational infrastructure. You can’t build a car without a wheel, or a smartphone without CPUs. You need the foundational infrastructure for technology to advance. As the saying goes, you must first walk before you can run. Secondly, innovation requires long-term investment. It usually takes years of investing up front before seeing any significant ROI. To make matters worse, your investment may not even work. Your customers may not adapt to the innovation, or it may not be worth the required price increase.

When an innovation is successful, the company and society reap massive rewards. The company gains market share or increases profit margins, and customers get an even better product. Electric vehicles (EVs) have been around since 1830 and competed with gasoline cars until Ford’s internal combustion engine (ICE) cars became too efficient and affordable for EVs to compete. The reason ICE cars beat EVs at the time was that they had infrastructural advantages that propelled their success. Electricity was not yet widely available outside city centers, severely limiting the market for cars tied to that infrastructure. For ICE cars, drivers could carry spare cans of gasoline for long journeys. By the mid-1900, most EVs either converted to ICE or went bust. The few that remained kept experimenting because of some promising advantages to EVs: they have more torque and fewer moving parts which makes them more reliable and easier to maintain. Since so few manufacturers ventured into EVs, there was not enough capital or resources invested into the technology for the batteries to develop.

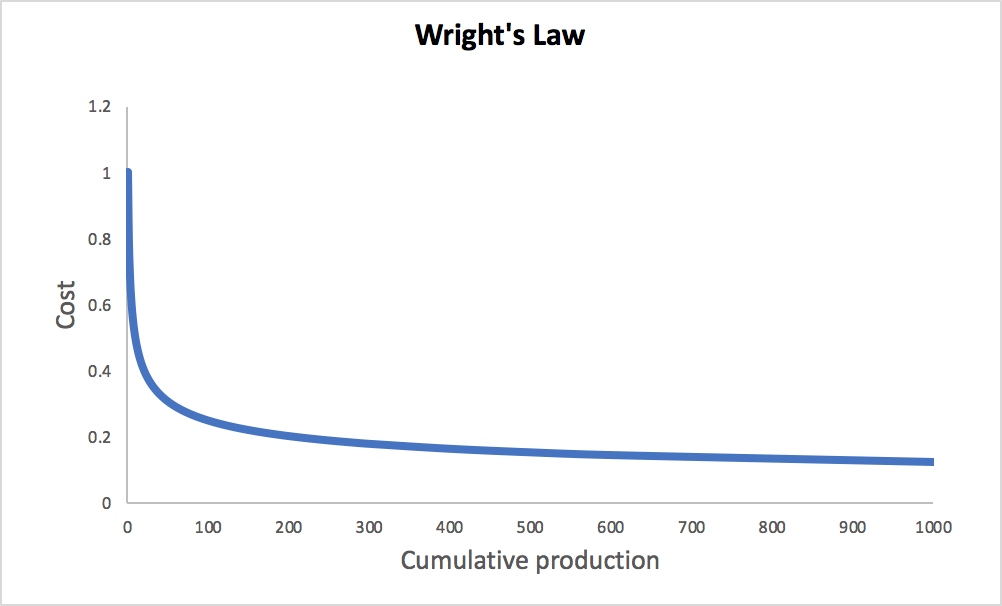

Wright’s law explains this situation down to a tee. Wright’s law states that progress increases with experience: Each percentage increase in cumulative production in a given industry results in a fixed percentage improvement in production efficiency. So due to infrastructural hurdles, EVs were not produced as much as ICE cars. As cumulative ICE production increased, so did its production efficiency and innovation, furthering the gap between EV and ICE efficiency. Since 2008, Tesla Motors focused all its capital and resources on EVs and managed to build a product appealing enough to sell which attracted investors. With the extra capital of investors, Tesla was able to increase production and R&D. Through that, they have made massive improvements to lithium-ion battery efficiency such as range, safety, charge time, and life cycle. In addition to improving battery technology, they have helped cultivate the investment into self-driving technology, over-the-air (OTA) software updates, and the supercharger network. EVs have actually always been quicker, more efficient, more reliable, and of course more eco-friendly than ICEs, but due to Wright’s law and the nature of business (profit or die), it took a while to develop. EVs are now finally making their way to their rightful place as the mainstream car.

Wright’s law was actually determined while studying airplane manufacture—for every doubling of airplane production the labor requirement was reduced by 10-15%. The law can be used to predict the prices of products in many different industries.

All of this makes me wonder what amazing technology we have out there that is either exclusively available to certain people, or on standby until it is financially viable to manufacture. It is possible that we already have lightning-fast internet, flying cars, war drones, and even a time machine, but due to the nature of business and supply chain, we just don’t have access to it… yet.